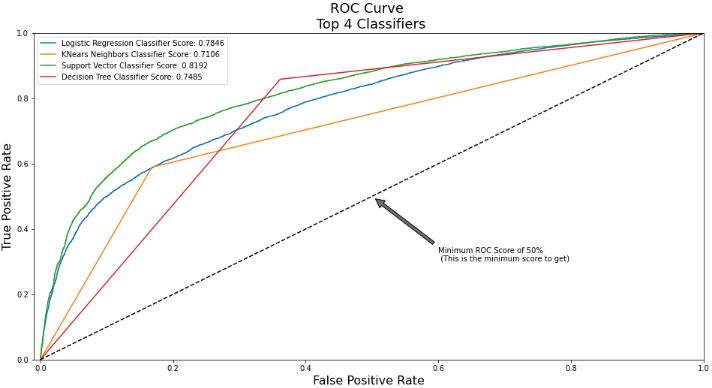

If presented with two customers with their respective profiles, how do you determine who will get a loan? The goal of this project

was to build a model that lenders can use to help make the best financial decisions regarding the customers to lend and those

not to lend. Therefore, the main goal is to build a state-of-the-art credit scoring model by predicting the probability that

somebody will experience financial distress in the next two years. This is a binary classification problem with classes; 0 :

Not deliquent & 1: Deliquency (Kaggle Challenge).

Algorithms : Logistic Regression, Random Forest, Decision Trees and k-Nearest Neighbors

How can the task of face detection be achieved? On this topic, earlier studies have proposed a framework for face detection

based on multi-task cascaded CNNs. Experimental results and my other proposed framework show that my MTCNN techniques

consistently outperform most of the main techniques. The second experiment is likewise accomplished using the Haar cascade

set of rules on my dataset.

Algorithms : Convolutional Neural Network, MTCNN, Haar Cascade

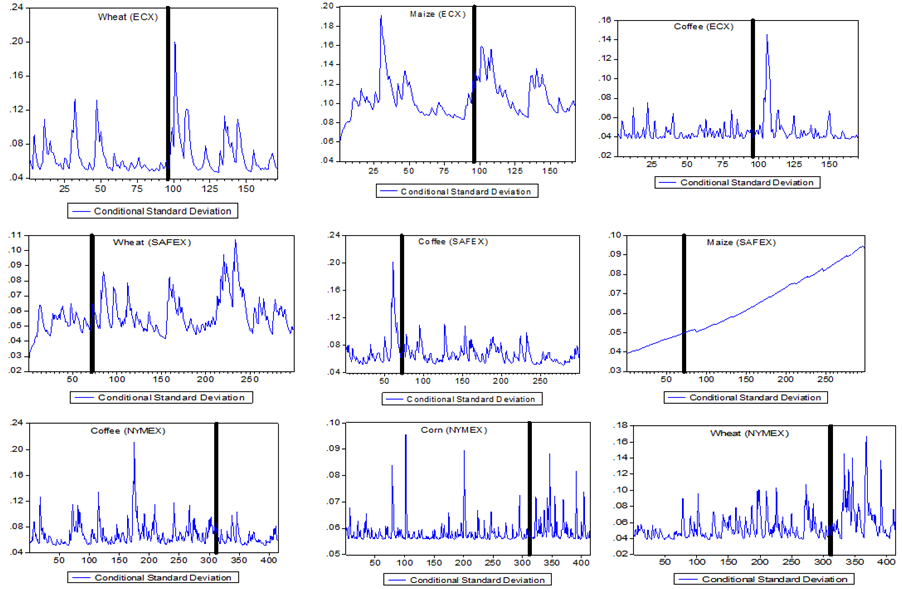

This study examines the impact of introduction of futures trading on the spot price volatility in the commodity

market. The paper considers the United States of America, South Africa and Ethiopian economies. Three commodities i.e.

coffee, maize and wheat from New York Mercantile Exchange, South African Futures Exchange and Ethiopian Commodity

Exchange are analyzed. ARCH LM test is used to check for heteroskedasticity and GARCH and EGARCH are used to check for

the behavior of volatility for the pre- and post-futures periods. This paper has focused on the overlooked factor by

earlier researchers, i.e. of economic-gap amongst countries, in looking at the impact of the futures trading on the

spot price variation.

Keywords: derivatives, futures exchange, agricultural commodities, spot price volatility

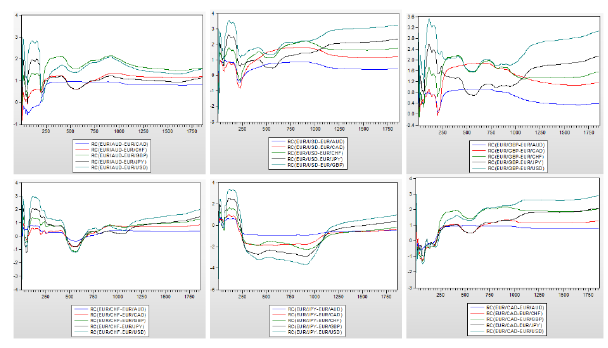

With the advent of high frequency data, the sum of squared returns between trades which is the most common estimator,

is biased by microstructure effects like bid-ask bounce thus the need to drop most of the data. Nonetheless, a number of

alternative estimators that make efficient use of the available data have been developed. However, choosing an estimator is

not trivial since the study of their relative merits focuses on the speed of convergence to their asymptotic distributions.

The paper is an effort towards estimating a covariance matrix using high-frequency data (quadratic covariation) from the

portfolio selection perspective. Covariance matrices based on intraday returns were constructed and evaluated.

Keywords: High Frequency Data, QMLE, Portfolio Optimization, Covariance Matrix

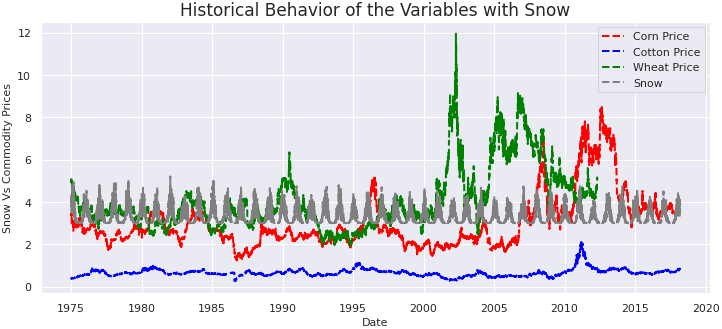

The study was conducted across three agricultural commodities, namely; corn, cotton and wheat against a number of weather

variables, including; temperature, rainfall, precipitation, sea level pressure, snow, fog and hail. This is after dropping

a number of weather variables that are highly correlated from the correlation matrix. The results indicate significance of

these exogenous variables in explaining the price variations as seen from the p-values of 0.00 across the three commodities.

The SARIMAX prediction also did well for Corn and Cotton prices as seen by the sufficiently high r2 score as opposed to the

estimate gotten from wheat. (Yet to study the same applying AI techniques).

Keywords: SARIMAX, Weather Shocks, Price Volatility

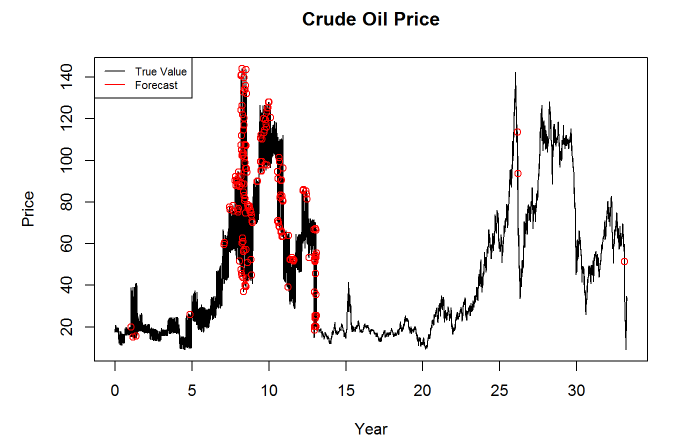

Energy remains an essential pillar for human livelihood for its necessity in sustainability and development of any current

civilization. One of the main feature distinguishing it from most of the other commodities is the mean-reverting characteristic

together with evident spikes and high volatility as seen for electricity and crude oil prices. A number of works have employed

the Ornstein–Uhlenbeck process to model directly the dynamics over time of different commodity spot prices under reduced-form

one-factor models (Ribeiro and Hodges, 2004). Nonetheless, in recent studies, crude oil spot price has also been modelled as

a jump-diffusion process, as attributed to Merton (1976), as in Jorion (1988) and Ball & Torous (1983).

Keywords: Crude Oil Price Modeling, Jump-diffusion models, Poisson process

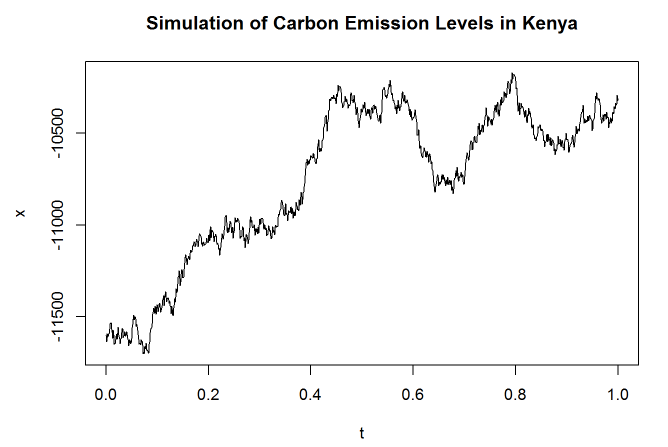

Energy remains an essential pillar for human livelihood for its necessity in sustainability and development of any current

civilization. Here, we derive the analytical solution to the stochastic differential equation for the Ornstein-Uhlenbeck process:

dXt=κ(θ−Xt)dt+σdWt where the Wt is a standard wiener process, and κ>0, θ and σ>0 Motivated by the observation that θ is

supposed to be the long-term mean of the process Xt, we can simplify the above SDE by introducing the change of variable;

Yt=Xt−θ that subtracts off the mean. The Yt satisfies the SDE; dYt=dXt=−κYtdt+σdWt for this SDE, the process Yt is seen to

have a drift towards zero value, at an exponential rate κ. This motivates the change of variables; Yt=e−κtZt ⇔ Zt=eκtYt,

which should remove the drift.

Keywords: O-U process, Carbon emission

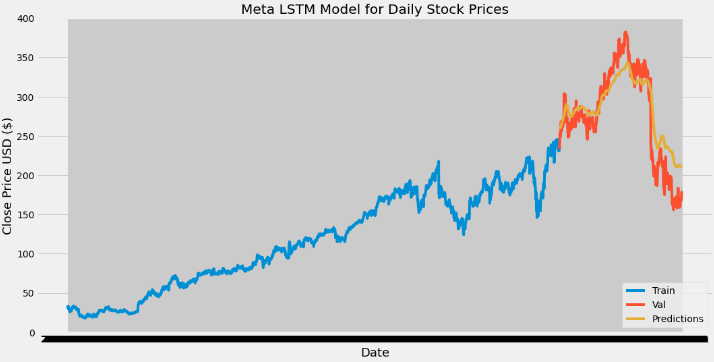

This project is an attempt at forecasting the stock prices for Apple (AAPL), Microsoft (MSFT) and Meta (FB) with the use of the

Long Short-Term Memory (LSTM) neural network. The data was extracted from Yahoo finance for daily, weekly and monthly intervals’.

Apple and Microsoft stock prices covered the period from 01-01-1999 to 12-08-2022 while the Meta data available covers from

19-05-2012 to 12-08-2022. The forecasting was done with use of the closing stock prices for the respective time frequency. The

testing result confirm that our model is capable of tracing the evolution of opening prices for both assets. Future work on the topic

could try more range of hyperparameter tuning (number of epochs and batch sizes) to get to the global minima of the loss

function and check for any improbvements in the model accuracy.

Keywords: Time Series, LSTM, RNN